Something changed on the battlefields of Ukraine — and it's not going back. A $500 drone started taking out tanks worth a hundred times more. That single lesson forced every defense ministry on earth to rethink how wars get fought. It also kicked off one of the biggest investment booms in a generation.

Then came February 28, 2026. The United States and Israel launched strikes on Iran. Iran hit back with drone swarms across nine countries at once. And overnight, the world got a live demonstration of what the next generation of drone warfare actually looks like — at scale, in real time, with real consequences.

If you're running strategy at a defense contractor, managing a fund with defense tech exposure, or selling into this market, the opportunity is real and it's right now. The problem is the data you need to act on it — who's raising, who just won a contract, who's quietly entering a new market — is scattered everywhere. It moves fast. And if you're still relying on quarterly reports and Google alerts, you're already behind.

That's the exact gap Webnyze was built to fill. In this piece, we break down the current state of the military drone market, where the money is going, how the 2026 Middle East conflict is reshaping procurement, and how teams are using structured web data to make sharper decisions in one of the fastest-moving sectors out there.

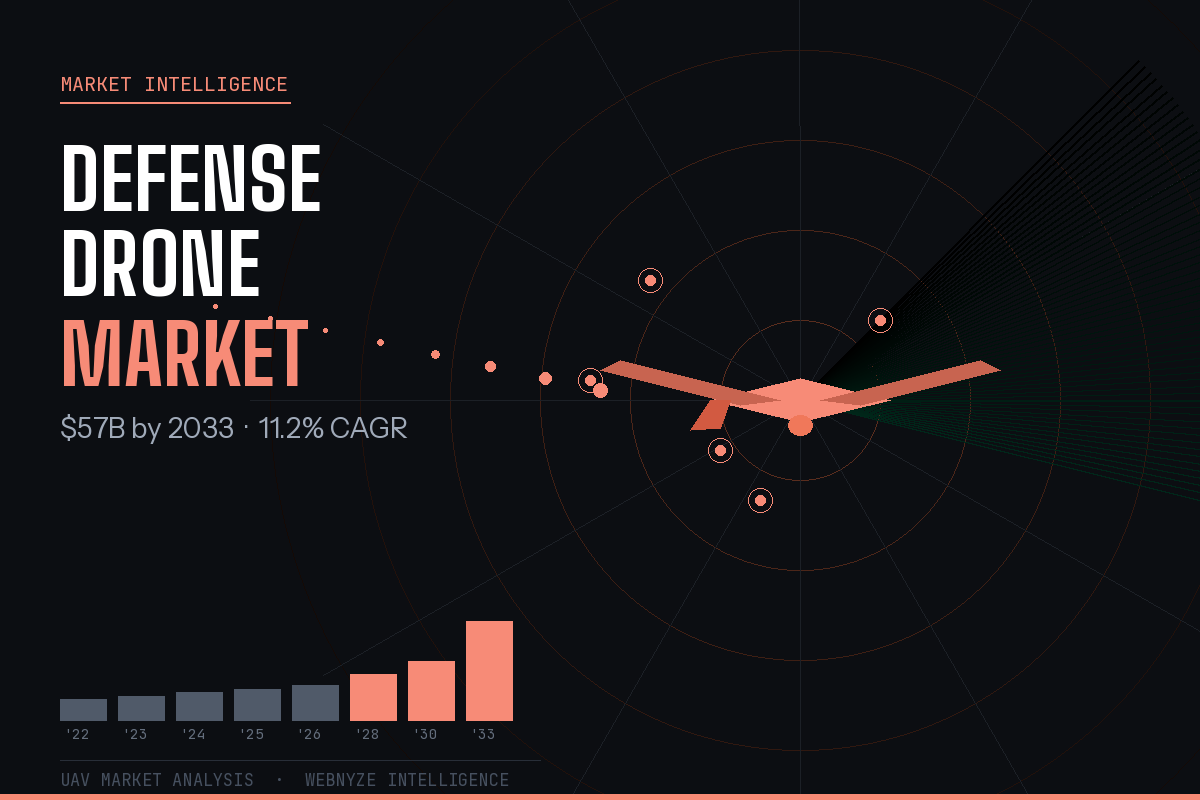

The numbers tell a clear story. The military drone market sat at around $16–18 billion in 2025. By 2033, it's expected to hit $57 billion at an 11.2% compound annual growth rate. That's not a niche projection from a single analyst report — multiple independent research firms are converging on the same trajectory, driven by the same underlying forces: rising defense budgets, geopolitical instability, and battlefield proof that drones work.

Ukraine proved it beyond any doubt: a $500 drone can destroy a $5 million tank. When a Russian drone entered Polish airspace in September 2025, NATO scrambled multimillion-dollar jets to chase something that cost less than a used car. That kind of mismatch isn't just embarrassing — it's forcing every defense ministry to rewrite its playbook from scratch.

Europe got the message fast. The EU's ReArm Europe plan is mobilizing up to €800 billion into defense, with drones and counter-drone systems at the top of the spending list. NATO agreed in June 2025 to push spending targets to 5% of GDP by 2035 — the most ambitious collective rearmament in the alliance's history. Poland is already there, at 4.7% of GDP in 2025, the highest of any member. The European Commission launched a €150 billion SAFE loan instrument aimed squarely at drone capabilities, and five major NATO powers have joined the LEAP program to co-produce autonomous strike drones together.

Across the Atlantic, the DoD earmarked $1.8 billion in FY2025 for autonomous unmanned systems — up 24% from the year before. The Collaborative Combat Aircraft program is fielding AI drone wingmen to fly alongside manned jets. General Atomics' YFQ-42A took its first flight in August 2025. Anduril's YFQ-44A followed on Halloween. Both are already past "experimental."

One deal that shows the real scale: in July 2025, the Pentagon gave Auterion $50 million to supply 33,000 AI drone guidance kits to Ukraine. Each kit turns a basic FPV drone into a system that can autonomously identify and hit a target up to a kilometer away. This is operational technology, deployed at scale, today.

2025 was the year Silicon Valley stopped pretending it had ethical objections to defense. VC funding for defense startups more than doubled — from $7.3 billion in 2024 to $17.9 billion — with the number of firms writing checks growing 41%. The old ESG-driven reluctance got reframed as "investing in democratic values," and the wallets opened.

The biggest rounds tell the story. Anduril, Helsing, and Saronic led the pack for the second year running. Anduril is reportedly mid-raise on a $4 billion round at a $60 billion valuation, led by Andreessen Horowitz and Thrive Capital — one of the largest private rounds in defense history. They'd already closed $2.5 billion from Founders Fund in June 2025. Shield AI hit a $5.6 billion valuation after its $240 million Series F-1 in March 2025. German firm Helsing raised €600 million in a Series D, valuing it at €12 billion.

| Company | Total Funding | Valuation | Key Product | Segment |

|---|---|---|---|---|

| Anduril Industries | $6.26B+ | ~$60B (est.) | Lattice OS, Fury YFQ-44A | Combat UAV |

| Shield AI | $1.3B+ | $5.6B | V-BAT, Hivemind autonomy | Autonomous ISR |

| Helsing | €600M (Series D) | €12B | Battlefield AI software | Defense AI |

| AeroVironment | Public (AVAV) | $20B+ pipeline | Switchblade loitering munitions | Loitering Munition |

| Tekever | Unicorn (2025) | Unicorn status | AI-powered surveillance drones | ISR |

| Skydio | Series E+ | $2.2B+ | X10, NDAA-compliant UAVs | Dual-Use |

| Saronic Technologies | $175M (Series B) | $1B+ | Autonomous surface vessels | Maritime UAS |

The market breaks into distinct categories, and the money isn't moving equally across all of them. Knowing which segments are attracting the most capital and contracts is exactly the kind of intelligence that separates reactive players from first-movers.

ISR drones own the largest market slice right now. Every military wants persistent eyes in the sky — for borders, battlefields, and finding targets before the other side does. Fixed-wing platforms account for over 66% of military drone revenue because they fly longer, fly higher, and cost less per hour than any alternative.

This is where the growth story sharpens. The combat drone market — UCAVs and loitering munitions — hit $8.2 billion in 2024 and is heading for $15.5 billion by 2032 at an 8.3% CAGR. AeroVironment's Switchblade got deployed at scale in Ukraine and proved the concept works. Precision strike on a limited budget — every military wants it now, not in five years.

This is the segment to watch most closely. Military AI spending hit $10.4 billion in 2024 and is compounding at 13.4% per year. Shield AI's Hivemind — which keeps drones flying autonomously when GPS is jammed — has logged over 170 combat sorties in Ukraine. Their V-BAT drones identified more than 200 Russian targets in 2025 while operating in fully contested airspace. That's not a demo anymore. That's a product in field production.

If Ukraine validated drone warfare as a concept, the 2026 Middle East conflict has stress-tested it at a completely different scale. On February 28, 2026, the US and Israel launched Operation Epic Fury — a coordinated campaign targeting Iran's nuclear infrastructure, military command, and top leadership. Iran's response didn't just hit Israel. It hit nine countries at once.

For anyone tracking the defense drone market, this is not background noise. It's a live procurement signal, a technology validation test, and a real-time stress test of every major drone system in active service — all simultaneously.

Iran's weapon of choice is the Shahed — a cheap, one-way attack drone used by Iran and its proxies since 2022. In the 2025 Twelve-Day War alone, Iran launched over 1,000 Shahed-class drones alongside 550 ballistic missiles. In 2026, the same playbook went regional: simultaneous drone and missile barrages across Bahrain, Kuwait, Qatar, Saudi Arabia, the UAE, Jordan, and a UK RAF base in Cyprus.

The logic is cold and deliberate: flood the skies with cheap drones, drain the expensive interceptors. Israel's Iron Dome, David's Sling, and Arrow systems are built exactly for this — but each interceptor costs orders of magnitude more than the drones they shoot down. Iran is turning cost asymmetry into a strategic weapon. It's working.

The most significant tactical move of this conflict is the US deploying Shahed-style one-way drones for the first time in American military history. Combined with Tomahawk cruise missiles, B-2 and B-1 bomber runs, and HIMARS precision missiles, the US hit over 1,000 targets inside Iran in the first 24 hours. By day ten, Iranian drone and missile output had dropped more than 90% — a result of systematically destroying launchers, storage sites, and command nodes before they could be used.

Before the first public strike of the 2025 Twelve-Day War, Israeli intelligence had already placed a covert drone base near Tehran. That network disabled Iranian air defenses and secured air superiority before a single manned jet entered Iranian airspace. The opening operation killed 30 Iranian generals and nine nuclear scientists in minutes. ISR drones didn't fire a shot — they just made sure everything else could. That's how consequential this category has become.

Israeli interceptor stockpiles were already strained after 2025. The 2026 campaign has triggered emergency procurement across NATO-aligned defense ministries. Replenishment contracts will run for years at minimum.

The US deploying Shahed-class drones isn't an experiment — it's a doctrine shift. Every allied military will now want a cheap, expendable attack drone program. That's an entire procurement category that barely existed 24 months ago.

Covert ISR drones decided the opening phase of the conflict before the public saw a single strike. Defense ministries watching this will accelerate ISR satellite and drone programs — the category that space and defense contractors are scaling hardest into.

Emergency procurements, accelerated tenders, and new program authorizations are being issued right now. Teams without live contract monitoring are already behind. This is exactly the gap Webnyze was built to close.

This market moves in days. A contract award, a funding announcement, or a key executive hire at a competitor can shift the whole picture overnight. If your team is still piecing things together from press releases and LinkedIn, you're seeing last week's picture while your competitors are working on today's.

That's why defense-sector clients come to us. Webnyze turns the chaos into structured, queryable data. Here's what that actually looks like in practice:

Webnyze continuously scrapes company profiles, funding signals, investor participation, and valuation changes across defense tech. When Anduril closed its $2.5B round in June 2025 or when Shield AI's $240M Series F-1 dropped, clients had structured, queryable data within hours — not days. Investment teams use this to build target lists, track competitor growth, and spot acquisition opportunities before they become news.

Defense contracts and procurement announcements are buried across thousands of press releases, government portals, and regulatory filings. Webnyze extracts and structures this signal — contract values, awarding agencies, vehicle types, expiry dates — into clean datasets. When the US Army awarded contracts to Anduril and Performance Drone Works for ISTAR drones in September 2024, clients on our defense contract feed had it tagged and structured the same business day.

Procurement decisions are made by people — not organizations. Webnyze maps senior executives, program officers, BD leads, and board members across the drone sector, including career histories and government affiliations. For a BD team targeting DoD contracts, knowing who moved from DARPA to Anduril or which procurement officer just joined Skydio is worth more than most financial metrics.

Data doesn't win deals. What you do with it does. Here's how teams across the defense drone space are putting this intelligence to work right now:

Defense contractors use company intelligence to track which startups are gaining DoD traction, watch competitor product announcements in real time, and spot partnership gaps before they become vulnerabilities. Knowing Anduril acquired Klas in July 2025 before a competitor does is a small example of the edge this creates.

VC and PE funds use Webnyze funding data to cross-reference stated company metrics against actual contract awards, flag discrepancies, and identify undervalued targets before formal fundraising processes open. By the time a process launches, the informed investors already have context on everyone in the room.

Companies entering European defense markets use contract and news data to identify which procurement vehicles are active, which countries are accelerating drone spending, and which local partners already have relationships with key ministries. The SAFE instrument and LEAP program alone represent years of contract flow for those who position early.

BD teams use people data to map decision-makers at defense agencies, track org chart changes, and monitor executive movement — then build relationships before procurement cycles open, not during them. The difference between being on a vendor shortlist and finding out about a contract after it closes often comes down to a six-month head start.

The pace isn't slowing. These are the four developments we think matter most for the rest of the year:

Europe is building its own drone industry — fast. The SAFE instrument and the LEAP program together are the biggest coordinated European drone procurement ever attempted. If you're a supplier positioning into this market, or you help clients understand who's winning contracts, this is a once-in-a-decade window that's already open.

Software is the real moat now. Hardware is getting commoditized. The battle has shifted to the AI stack on top. Platforms like Shield AI's Hivemind and Anduril's Lattice OS are what every major prime wants to license. Tracking which defense contractors are adopting these platforms — and for which programs — is an intelligence gap most organizations haven't closed yet.

The M&A wave is just beginning. Defense tech exits hit $54.4 billion in 2025, nearly tripling from the year before, mostly through acquisitions. Companies mapping acquisition targets today — using real-time funding, people, and contract data — will close deals while everyone else is still doing research. The window between "interesting company" and "already acquired" is shrinking.

Asia-Pacific is the sleeper market. APAC is projected to drive 36% of global military drone market growth through 2030. India, South Korea, Japan, and Australia are all expanding procurement programs significantly. If you don't have visibility into procurement signals from this region yet, you're building a blind spot that compounds every quarter.

The military drone market is one of the defining investment stories of this decade. The money is real, the geopolitical drivers are locked in, and the technology is being battle-tested every single day — right now, in real conflict zones, against real adversaries.

But fast-moving markets punish slow information. The teams winning right now aren't the biggest. They're the ones with the cleanest data. They know who's raising before the press release. They know which decision-makers just changed roles before LinkedIn updates. They know which contracts went live before competitors start writing proposals.

At Webnyze, we take the noise — the scattered press releases, government portals, funding announcements, and people moves — and turn it into structured, queryable intelligence delivered where your team actually works. No more stitching spreadsheets from five different sources. Just the data, ready to use, at the speed this market demands.

Request a free sample dataset covering defense drone companies, funding rounds, and live contract signals — or talk to us about a custom scraping solution built around your intelligence needs.

Tell us what you need to scrape. We'll deliver a free sample dataset within 48 hours — no commitment, no credit card.