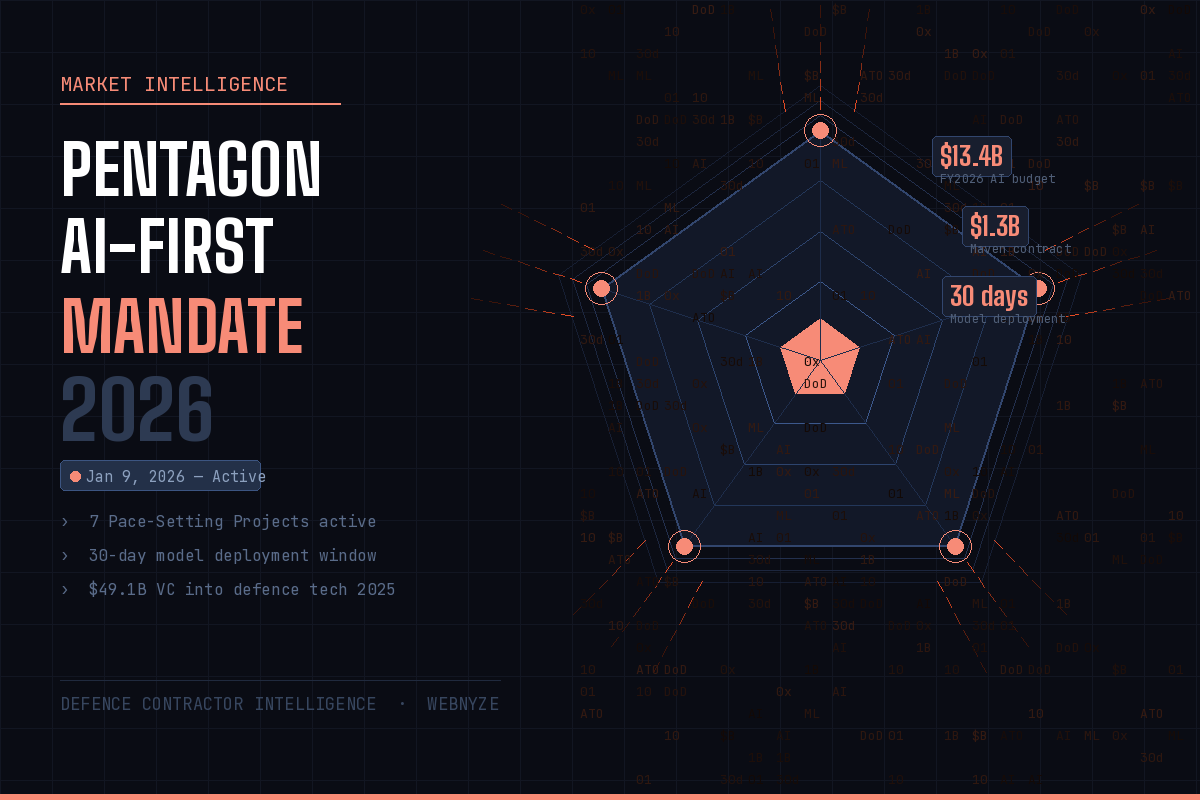

The date that will mark a before-and-after for US defence procurement is January 9, 2026. That's when Secretary Pete Hegseth signed two memoranda that, taken together, constitute the most significant shift in how the Pentagon acquires technology since the creation of the Defense Innovation Unit a decade ago. The AI-First mandate doesn't just encourage AI adoption - it mandates it, with measurable timelines, a single designated CTO with real authority, and a 30-day deployment window that requires the latest commercial AI models to be in the hands of military users within a month of their public release.

The implications for defence contractors are not theoretical. In the weeks that followed, Palantir's Maven Smart System was elevated to a permanent program of record - locking in multi-year funding for the AI targeting platform already deployed across every US combatant command. Shield AI raised $2 billion at a $12.7 billion valuation after its Hivemind autonomy software was selected for the Air Force's Collaborative Combat Aircraft programme. Anduril's $20 billion enterprise contract vehicle with the Army opened a procurement pathway for counter-drone and autonomy capabilities that any federal agency can now draw from. And OpenAI signed a deployment agreement with the Pentagon for classified environments, just weeks after Anthropic's withdrawal.

What's easy to miss in the avalanche of contract announcements and funding rounds is the underlying pattern: the DoD is spending $13.4 billion on AI in FY2026 alone, moving faster than any traditional procurement cycle was designed to handle, and the winners are the companies who knew where the money was going before the solicitations were published.

That information gap - between when a requirement is shaped and when a formal contract is announced - is where data intelligence becomes the decisive edge. This piece breaks down exactly what the AI-First mandate means for the defence industrial base, which companies are positioning most effectively, and how BD and strategy teams are using structured procurement data to stay ahead of a cycle that moves in days rather than quarters.

The January 9 memoranda are worth reading carefully, because they are not the usual policy language. Secretary Hegseth's framing is unambiguous: "We must accept that the risks of not moving fast enough outweigh the risks of imperfect alignment." The Artificial Intelligence Strategy for the Department of War sets out measurable commitments rather than aspirational goals. Seven Pace-Setting Projects, each with specific timelines. A 30-day deployment window for new AI models. A Barrier Removal Board with authority to waive non-statutory requirements. A Wartime CDAO directed to treat data-sharing blockers and ATO delays the way a wartime commander treats supply chain failures.

Three changes are structurally significant for anyone doing business with the DoD.

The first is the 30-day model deployment criterion. The mandate requires that the latest commercial AI models - GPT-5, Claude, Gemini, whatever ships next quarter - be available to military users within 30 days of public release. That is a procurement criterion, not just a deployment goal. It means contracts that were designed to lock in a specific model version are now structurally non-compliant. Any vendor whose product architecture can't update continuously is at a disadvantage going forward, regardless of past performance.

The second is the designation of a single DoD CTO with real authority. Previously, innovation-seeking companies had to navigate DARPA, the Defense Innovation Unit, the Chief Digital and AI Office, individual service branches, and combatant commands - often running what Hegseth himself called "endless laps" before finding a willing buyer. A single CTO with decision authority across all of those structures changes the targeting calculation for BD teams entirely. There's now a clearer acquisition pathway, but also a more concentrated decision-making node whose priorities and programme focus are worth tracking closely.

The third is what the mandate does to OTA pathways and unsolicited proposals. The language explicitly encourages unsolicited proposals for innovative AI tools that find "receptive audiences." Other Transaction Authority has been expanded, and the Barrier Removal Board was created specifically to unblock contracting mechanisms that slow down non-traditional vendors. For companies without legacy defence relationships, this is the first time in a decade that the structural barriers to entry have genuinely shifted.

The initial PSPs span Warfighting (autonomous battle management), Intelligence (sensor fusion, AI targeting), and Enterprise (AI for acquisition, logistics, finance). Companies engaged in PSPs gain first-mover advantage in the larger programmes that follow each one.

Any contract that locks in a specific AI model version is now structurally non-compliant with the mandate. Vendors must demonstrate continuous update capacity. This is a direct structural advantage for software-first companies over traditional primes.

The Under Secretary for Research & Engineering now has DoD-wide AI authority. For BD teams, this simplifies the entry question - but it also means the wrong relationship with one decision-maker matters more than before.

A monthly board with authority to waive non-statutory requirements. For non-traditional vendors and startups, this is the most significant structural change in DoD acquisition in a decade. OTA pathways are actively expanding.

If you want to understand where the DoD's AI procurement is heading, you follow Project Maven - not because it's the only programme that matters, but because it is the blueprint that every subsequent AI programme is being modelled on. Maven began in 2017 as an effort to apply machine learning to drone surveillance footage. Google was the original partner, withdrew in 2018 after employee protests, and Palantir stepped in. What has happened since is the fastest transformation of an experimental government technology programme into core military infrastructure in modern memory.

The contract history tells the story. Palantir received $480 million for a five-year IDIQ in May 2024 - covering five combatant commands. By May 2025, the ceiling was raised to $1.3 billion through 2029, driven by what officials described as adoption "far greater than expectations." By September 2025, Maven was deployed across every unified combatant command - CENTCOM, EUCOM, INDOPACOM, NORTHCOM, SOCOM, and the rest. More than 20,000 active users across 35 military software tools, with the user base having quadrupled from March 2024 to mid-2025.

Then, on March 9, 2026, Deputy Secretary Steve Feinberg signed the directive that moved Maven from a procurement programme to a permanent program of record - meaning dedicated budget lines, inclusion in the five-year Future Years Defense Program, and institutional protection from the annual budget cycle. "Being designated as a program of record means Palantir's MSS is now in as permanent a position as a program can get within the DoD," as one analyst put it bluntly.

During the 2026 US-Israel-Iran conflict, Maven's operational significance became impossible to ignore. The system enabled the targeting of over 1,000 Iranian sites in the first 24 hours of Operation Epic Fury. Cameron Stanley, the Pentagon's Chief Digital and AI Officer, said at AIPCon 9 in early 2026 that Maven was being "deployed across the entire department." The AI Asset Tasking Recommender - a module that proposes which bombers and munitions should be assigned to which targets - processed targeting recommendations at a rate the DoD had never achieved manually. By June 2026, 100% machine-generated intelligence is planned to begin flowing to combatant commanders.

NATO has since adopted Maven directly - the NCIA finalised a contract for Maven Smart System NATO in March 2025, with deployment across Allied Command Operations completed by August 2025. Maven is now the de facto AI backbone of both the US military and NATO alliance operations simultaneously.

What this means for contractors is not that Palantir has won forever. Maven's architecture is explicitly designed for integration - Palantir has stated that their intent is to incorporate any new sensor or AI capability the government acquires. The programme is, in a sense, the procurement vehicle through which the rest of the AI-First mandate gets implemented. Every new AI capability that needs to integrate with DoD command and control will need to be Maven-compatible.

$13.4 billion in a single fiscal year makes the DoD the largest AI procurement programme on earth. Understanding how that budget breaks down - and which segments are growing fastest - is the foundational intelligence task for any contractor positioned in this market.

The largest single category is aerial autonomous systems at $9.4 billion - reflecting the Collaborative Combat Aircraft programme, the Replicator drone initiative, and the full range of autonomous UAV programmes across the services. Maritime autonomy takes $1.7 billion. AI/ML software integration - the layer that includes Maven, Lattice, Hivemind, and the software defined by the MOSA requirement - is $1.2 billion in direct software spending, though the real number is substantially higher when hardware contracts with embedded software are included.

The $1.8 billion allocated to autonomous unmanned systems specifically represents a 24% increase from FY2025 - and that was itself a significant increase. The compounding rate of growth in this category is the clearest signal of where procurement attention is concentrating. For contractors not already positioned in autonomous systems, the question is not whether to move into this category but how fast.

The story of who is winning in the AI-First DoD is also the story of what the defence industrial base is becoming. The traditional prime contractor model - Lockheed, Raytheon, Boeing, Northrop, building vertically integrated hardware platforms over decade-long programme cycles - is not disappearing. But it is being structurally disrupted by software-first companies whose economics, development speed, and AI architecture are fundamentally different.

Shield AI's Hivemind is the world's first autonomous AI pilot used continuously in combat since 2018. Its core innovation is operating without GPS, communications links, or human control - specifically designed for denied, degraded, intermittent, or limited-bandwidth environments that electronic warfare creates. In February 2026, the US Air Force selected Hivemind for its Collaborative Combat Aircraft programme - the most significant autonomous aviation contract in a generation. In the same month, Hivemind was tested switching with Anduril's Lattice AI on the same Fury aircraft mid-flight, successfully completing tasks with both. The Air Force explicitly structured this to avoid software vendor lock-in.

Shield AI raised $2 billion at a $12.7 billion valuation in March 2026 - a 140% increase in one year from $5.3 billion. Revenue is projected at $540 million in 2026, with 80% CAGR. The company's V-BAT drones have logged more than 200 combat missions over Ukraine since 2024, operating in conditions that crashed most Western systems. The X-BAT - a VTOL stealth fighter drone piloted entirely by Hivemind - is on track for its first flight by end of 2026.

Anduril's strategy is the most ambitious in the sector: build both the hardware and the software stack, then sell the combination as an enterprise platform rather than individual programmes. The Fury CCA drone is in serial production at Arsenal-1 in Ohio. The $20 billion Army enterprise contract vehicle for Lattice-based counter-drone capabilities means any federal buyer can now acquire Anduril's commercial products against pre-negotiated terms. The company is reportedly pursuing a $4 billion raise at a $60 billion valuation.

What makes Anduril strategically significant beyond its own programmes is its role as an integration layer. Lattice ingests data from 150+ sources. Hivemind was tested on the Fury aircraft - a competitor's software running on Anduril hardware. Maven-compatible integrations are in progress. Anduril is positioning itself as the DoD's preferred open-architecture platform, which means its competitive moat deepens with every new sensor or AI tool the DoD acquires from anyone else.

| Company | Valuation / Revenue | Key Product | Anchor Contract | Position |

|---|---|---|---|---|

| Palantir | $150B+ market cap | Maven Smart System | $1.3B DoD IDIQ (POR) | AI C2 infrastructure |

| Anduril | ~$60B (est. raise) | Lattice OS, Fury CCA | $20B Army C-UAS vehicle | Hardware + software platform |

| Shield AI | $12.7B · $540M rev | Hivemind autonomous pilot | USAF CCA programme | Autonomy software |

| OpenAI | $300B+ (private) | GPT-5, o3 models | DoW classified deployment | Foundation model provider |

| Epirus | Series C+ | Leonidas HPM system | DoD directed energy R&D | Directed energy defeat |

| Lockheed Martin | $120B market cap | F-35, LRASM, C-UAS | $10B USAF contract mod | Legacy prime adapting |

| L3Harris | $36B market cap | ISR, EW, communications | Multiple service contracts | ISR + comms prime |

The most structurally significant element of the AI-First mandate for the legacy defence industrial base is the strict enforcement of Modular Open System Architectures. MOSA is not new - it's been DoD policy for several years - but the January 2026 memo made it a hard requirement with enforcement teeth, not a best-practice recommendation. Every AI system procured under the new mandate must have modular interfaces and documentation sufficient for third-party integration. No proprietary lock-in.

For traditional primes, this is a direct threat to the business model that has sustained them for decades. Lockheed, Boeing, and Raytheon built their economic moats by owning the full stack of a platform - airframe, sensors, software, sustainment. If MOSA is enforced, a DoD customer can replace the software layer of a Lockheed platform with Hivemind or Lattice without Lockheed's involvement. The sustainment tail shrinks. The lock-in disappears.

For non-traditional vendors, MOSA is an invitation. The Air Force's CCA programme made this concrete - Hivemind ran on Anduril's Fury hardware, which competes directly with Shield AI's own X-BAT. Two competing companies' software ran on the same aircraft in the same programme. That is the MOSA mandate in operation, and it is exactly what the DoD said it wanted: best-of-breed components from multiple vendors assembled into capability rather than single-vendor systems.

The implication for BD strategy is that the question is no longer "which prime is running this programme?" but "which capability layer is my company competing for, and who are the other vendors in that layer?" Tracking this requires a different kind of intelligence - not just contract award announcements, but teaming agreements, capability demonstrations, programme office technical workshops, and the specific requirements language that appears in pre-solicitation notices.

The AI-First mandate has compressed the gap between requirement formation and contract award in ways the traditional BD cycle was not built to handle. Programme offices that previously took 18 months to go from requirement to solicitation are now under direct pressure to move in weeks. The Barrier Removal Board exists specifically to eliminate the procedural delays that give incumbent contractors their incumbent advantages.

The companies building durable positions in this market are not doing it by tracking SAM.gov more diligently. They are doing it by having continuous, structured visibility into the procurement intelligence that matters - programme office signals, competitor contract wins, executive movements, and pre-solicitation activity - assembled into a picture that their BD and strategy teams can actually act on.

AI-related defence contracts appear across SAM.gov solicitations, USASpending.gov award records, DoD daily contract announcement pages, DIU opportunity listings, and service-specific programme office channels - often simultaneously, rarely in the same format. Webnyze structures all of these into a single queryable dataset: contract values, NAICS codes, awarding agencies, vehicle types, and expiry dates extracted and normalised daily. When Anduril's $20 billion enterprise contract vehicle was announced in March 2026, clients tracking AI procurement had the task order details, vehicle structure, and eligible capability categories structured within hours of the DoD announcement - including details that weren't in the public summary.

In the AI defence sector, a competitor's Series G funding round is a procurement signal. Shield AI's $2 billion raise signals production-scale deployment of Hivemind across multiple platforms. Anduril's reported $4 billion raise signals Arsenal-1 capacity expansion ahead of CCA production. Webnyze monitors company announcements, investor filings, trade press, and programme office disclosures to give strategy teams continuous visibility into competitive positioning - not monthly summaries. When the USAF announced Hivemind's selection for CCA in February 2026, clients had the capability layer breakdown, teaming structure, and adjacent programme implications structured the same day.

The seven Pace-Setting Projects are being defined by specific people in specific roles at CDAO, the programme offices of each service, and the combatant commands. Those people have career histories, prior programme associations, and technical preferences that are legible if you're tracking them. Webnyze monitors executive movements between government and industry - DARPA programme managers joining defence startups, acquisition officials moving to advisory roles, programme officers appearing on conference panels before solicitation release. These are requirement-shaping signals, not noise. The best time to build a relationship with the person writing the MOSA requirements for the next autonomy programme is before those requirements are drafted.

Most defence contracts are preceded by pre-solicitation notices, Requests for Information, Sources Sought announcements, and programme office technical workshops - each of which signals intent weeks or months before a formal solicitation. Webnyze monitors these across all DoD channels and structures them by capability domain, programme office, vehicle type, and incumbent contractor. For the AI programmes emerging from the Pace-Setting Projects, these pre-solicitation signals are appearing faster than traditional BD cycles are designed to catch them. The 30-day model deployment requirement means the DoD itself is operating on compressed timelines - and the contractors who track the pre-solicitation environment are the ones who can respond credibly when a solicitation opens with a two-week response window.

Behind the funding announcements and contract awards, there are specific BD and strategy practices that separate the companies building durable positions in this market from the ones chasing solicitations they learned about too late.

The MOSA environment means the relevant competitive question is "which capability layer are we competing for?" rather than "which prime is running this programme?" Companies tracking this effectively build maps of which vendors own which capability layers across active programmes - sensor fusion, autonomy software, C2 interfaces, data architecture - and identify the white spaces before solicitations define them. This is a research task that requires structured data, not a SAM.gov search.

Every major defence tech fundraise in the past 18 months has been a procurement signal - Shield AI's $2B raise precedes CCA production contracts; Anduril's reported $4B raise precedes Arsenal-1 capacity scaling for DoD demand. VC and PE funds doing due diligence in this sector are using contract intelligence to cross-reference stated revenue trajectories against actual award records in USASpending.gov. The gap between claimed DoD relationships and verifiable contract history is often significant - and finding it before a term sheet is signed is exactly what structured data makes possible.

The seven PSPs are explicitly described as procurement models - companies engaged in them gain first-mover advantage in the larger programmes that follow. But PSP engagement happens through pre-solicitation dialogue, capability demonstrations, and technical workshops - not through formal solicitations. Companies tracking CDAO and programme office signals from the day the mandate was issued have had four months to position for PSP engagement before formal procurement opens. That is not a recoverable head start through harder SAM.gov monitoring.

Maven is the integration layer through which the AI-First mandate gets implemented across the DoD. Every AI product that needs to integrate with DoD C2 will need Maven compatibility. Companies that have documented their MOSA-compliant interfaces, established relationships with Palantir's integration team, and participated in Maven demonstration exercises are building competitive positioning that compounds over time. The window to establish Maven-compatible positioning as an early entrant rather than a follower is closing as the programme-of-record designation locks in the procurement architecture.

The AI-First procurement cycle is moving faster than any prior DoD modernisation effort. These are the four developments that will define the competitive landscape through the end of the year.

Maven program-of-record budget submission - September 2026. Feinberg's March directive requires Maven to achieve full program-of-record status by the close of FY2026 on September 30. This means a dedicated budget line will appear in the Future Years Defense Program for the first time - giving analysts and competitors their first clear view of the multi-year funding trajectory. The contract size growth pattern (from $480M to $1.3B in one year) suggests the FYDP number will be significantly larger than anything currently public.

CCA prototype phase contracts - Q2/Q3 2026. The Collaborative Combat Aircraft prototype phase is moving to full production contracts this year. Anduril's Fury is in serial production at Arsenal-1. Shield AI's Hivemind is selected as the software layer. The formal production contracts - which will lock in unit numbers, delivery timelines, and sustainment arrangements - are the most significant autonomous aviation procurement event of the decade. Every layer of the CCA supply chain is being competed right now.

Pace-Setting Project solicitations - ongoing. The seven PSPs are designed to move from concept to contract in months. Pre-solicitation activity for each is happening now through CDAO, programme office RFIs, and the DIU's commercial solutions opening pathways. Companies that haven't been tracking the PSP signals since January are starting from a significant disadvantage relative to those who have been in continuous dialogue with programme offices.

OpenAI's classified deployment expansion. OpenAI signed its classified environment deployment agreement with the DoD in March 2026, weeks after Anthropic's withdrawal. By June 2026, Maven is planned to begin transmitting 100% machine-generated intelligence to combatant commanders. The integration of frontier commercial LLMs into operational military AI systems - and the specific capability gaps that creates for data infrastructure, context management, and output structuring - is a procurement opportunity category that barely existed 12 months ago.

The AI-First mandate doesn't just change what the DoD buys. It changes how fast it buys, what contractual flexibility it expects, and who gets to compete. The Barrier Removal Board, the 30-day model deployment criterion, the single CTO with real authority - these are not cosmetic changes to a system that was always going to move slowly. They are structural shifts that reward companies with the intelligence infrastructure to position early and the agility to respond when solicitations open faster than traditional BD cycles were built to handle.

The companies winning right now - Palantir, Anduril, Shield AI, and the tier of smaller vendors building into the MOSA architecture beneath them - are not winning because they have better lobbyists or longer track records. They are winning because they had continuous, structured visibility into where the procurement was going before the solicitations were published. They knew about the Pace-Setting Projects before the announcement. They had relationships with the right programme officers before the requirements were written. They were Maven-compatible before it became a procurement criterion.

At Webnyze, we build that intelligence infrastructure - contract signal monitoring across SAM.gov, USASpending, and DoD announcement channels, competitor and funding intelligence across the defence AI ecosystem, and decision-maker tracking across the government-to-industry pipeline. If the $13.4 billion AI procurement cycle is a market you're positioning into this year, that's the foundation worth building now.

Request a free sample dataset covering DoD AI contract awards, defence tech company funding signals, and live procurement intelligence - or talk to us about a custom monitoring solution built around your target programmes and capability domains.

Tell us what you need to scrape. We'll deliver a free sample dataset within 48 hours - no commitment, no credit card.